|

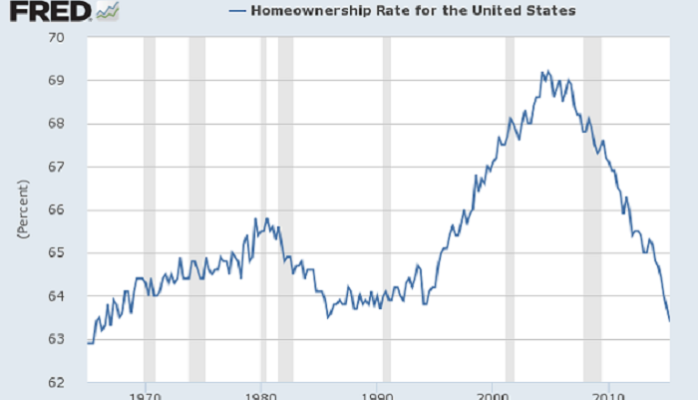

Let's begin with a quick explanation of how we got here. For the past 50 years, housing policy has relied on looser underwriting standards in an effort to increase homeownership and help the economy. Much of that lending has been targeted to low- and moderate-income homebuyers in an attempt to build wealth for these households. That agenda has pushed a reliance on high leverage, long amortization schedules (30-year loan terms), low down payments and high debt to income (DTI) ratios. In addition, these loans are often made to borrowers with impaired credit. That approach may have increased homeownership rates in the short term, but many homeowners could not handle their payments, and we are now seeing homeownership rates return to pre 1970 levels in the low-60-percent range. The push towards homeownership has neither increased the rates over the long haul, nor has it reliably created wealth.

After this push failed and the Great Depression took hold, lawmakers Barney Frank and Chris Dodd championed new legislation, called the Dodd-Frank Act (DFA), to prevent another financial debacle. The DFA greatly expands oversight and regulation of the financial institutions not seen since the Great Depression, and includes three criteria for housing finance reform: first, a high quality mortgage— called the Qualified Residential Mortgage (QRM)—that would have a minimal incidence of default; second, a set of minimum mortgage standards called the Qualified Mortgage (QM); and third, a requirement that the securitizer of any mortgage not a QRM retain at least 5 percent of the risk of any mortgage pool it sponsors. Unfortunately, politicians exerted their influence in defining QRM, which has resulted in a watered down version that only meets the minimum requirements of QM; in other words, the lending standards are looser and less safe than originally intended.

The National Association of Realtors and the general media have reported that the mortgage market is tight, and the Federal Reserve Chair, Janet Yellen, has stated that only people with pristine credit can get financing; neither statements are accurate. According to the American Enterprise Institute, there has been little discernible volume impact from the Qualified Mortgage regulation. Over the past three months, the DTI ratios are high, and a significant number of them were greater than 43 percent. Currently, the number of Fannie and Freddie loans that have total DTIs greater than 38 percent is more than double what they were in 1990. The Federal Housing Administration (FHA) has a sizable share of loans with DTIs over 50 percent, which is an extremely high pre-tax payment burden. That makes it difficult to pay income tax, commuting expenses, living expenses and food with what is left. The VA’s residual-income underwriting is a key to limiting defaults, and it’s unfortunate that Fannie Mae, Freddie Mac and the FHA do not look at this less risky method of analyzing ability to repay. The softness in mortgage lending is not due to tight standards, but to reduced affordability, loan put-back risk (part of DFA) and the sluggish economic recovery. The truth of the matter is that this recovery has had limited gains in income, and with an unequal distribution. It appears that our memories are short, and the financial lessons learned from the recent financial debacle are fading with the GSEs officially re-entering into the 97 percent LTV market. Currently, more than half of all purchase loans have a down payment of 5 percent or less. Under the original QRM proposed standards, borrowers would have been required to put 20 percent down. However, as noted above, that proposed standard disappeared under political pressure, as politicians and the real estate industrial complex have continued to push for looser lending standards – which, with an expanding credit box, will result in higher defaults. Even if a buyer can obtain financing, they should examine their true ability to repay, and may want to leave enough money to contribute to retirement plans and saving for their children’s education. Just because a lender will lend, does not mean that it is in the best long-term interest of the buyer. As a matter of fact, higher debt to income (DTI) ratios limit participation in defined contribution retirement plans such as 401(k)s, most of which come with employer matching contributions. Furthermore, having a high DTI often leads to insufficient income to meet the requirements of the mortgage, living costs and saving for the future. A 401(K) plan can be a reliable and attractive means for private wealth accumulation, particularly for the very groups that were the target of the increase in homeownership. Keeping the DTI to more affordable levels will allow for the unexpected household expenses that we all experience, and make it more likely to weather other financial upsets (such as losing a job). Share this post

John Agostinelli is the co-author of Easy Money and the American Real Estate Ponzi Scheme, and is a recognized authority in real estate. John is a real estate investor, broker, industry consultant and housing policy commentator. His market focus is the Boston MetroWest area.

He services: Ashland, Dover, Framingham, Holliston, Hopkinton, Marlborough, Medfield, Medway, Milford, Millis, Natick, Northborough, Sherborn, Southborough, Sudbury, Wayland, Westborough, Upton John has helped hundreds of investors, buyers and sellers, sell, purchase or invest in real estate in over 50 Massachusetts towns. Please contact him via email at [email protected] or by phone at 508-283-4958. Other helpful articles/books worth reading: http://www.easymoneyinamerica.com/ https://bostonagentmagazine.com/2015/01/19/the-short-list-john-agostinellis-tips-for-understanding-todays-financing-landscape/ http://www.gmnews.com/2016/08/11/housing-peaks-and-valleys/

1 Comment

Your comment will be posted after it is approved.

Leave a Reply. |

|

Coldwell Banker Lifestyles

603-823-8895 209 Main St, Franconia, NH 03580 Each office is individually owned and operated. |

© COPYRIGHT 2021. ALL RIGHTS RESERVED.